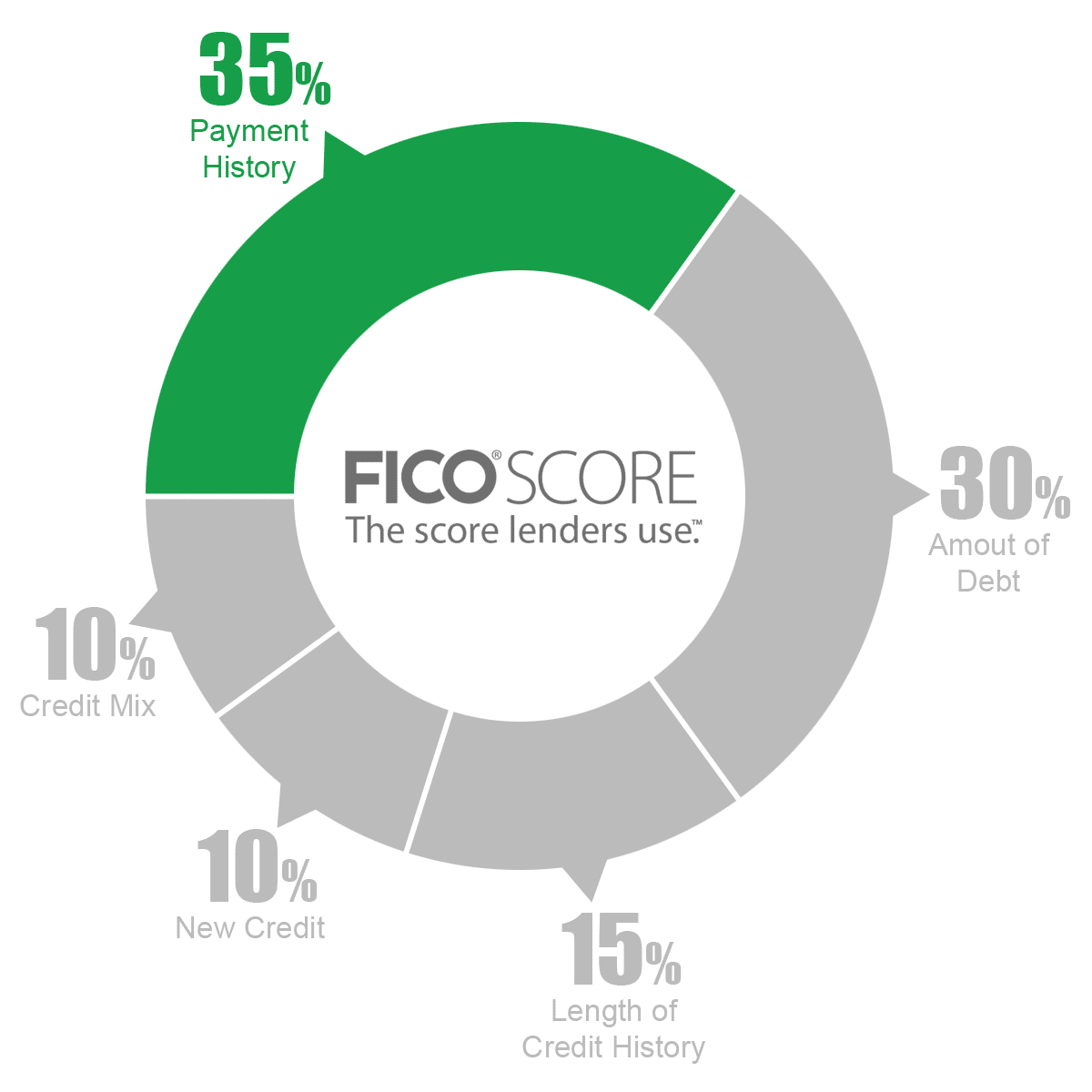

PAYMENT HISTORY

35% of Your Credit Score

Payment history is the most important part of your credit, accounting for 35% of your credit score.

Making late payments, encurring collections, charge-offs, or other derogatory information severely lowers your credit scores.

Paying your bills on time and putting together a payment history of on-time payments helps increase your credit scores.

What Accounts are Included in Your Payment History?

Payment history includes installment loans, revolving loans, collections, and public records.

Installment loans are loans with a fixed loan amount, monthly payment amount, and a set term.

For example, a $16,000 auto loan with a monthly payment of $309 a month for 60 months is an installment loan.

Some common installment loans are mortgages, auto loans, student loans, and personal loans.

Revolving loans have an open end term, a credit limit, and allow you revolve a balance from one month to another.

You may borrow money up to the credit limit and either pay the balance off at the end of the month or pay a portion of the balance and carry the remainder over to the next month.

The most common forms of revolving accounts are credit cards, lines of credit, and home equity lines of credit (HELOC).

Collection accounts are accounts reported by third party data furnishers who obtain past due debt from the original creditor.

Public records include tax liens, judgments, and bankruptcies.

Derogatory Accounts

Here is a list of of the negative items which will hurt your payment history and lower your credit scores;

Late Payments

Charge-offs

Collections

Accounts included in Bankruptcy

Foreclosures

Repossessions

Judgments

Tax Liens

Bankruptcies

Any of these accounts reporting on your credit reports will lower your credit scores.

Impact On Credit Scores

The last 6 months of your payment history carries the most weight when calculating your credit scores.

The last 24 months of your payment history carries the second most weight when calculating your credit scores.

Recent late payments, collections, and other derogatory accounts reporting within the last six months will hurt your credit scores more than older inactive accounts.

In fact, a collection account with a $0 balance active within the last six months can actually hurt your scores more than a three-year-old collection with a $300 balance.

This is why paying off collection accounts can sometimes lower your credit scores.

Disputing old charged-off accounts with balances that haven’t reported activity in over 2 years can also lower credit scores if the account is not deleted because the creditor will update the date last reported after the completion of the dispute.

Sometimes initiating debt validation or a document request directly with the creditor will be a safer way of working on removing the account, avoiding the risk of reactivating the date last reported.

Why Choose CreditFirm.net?

Assurance. Our Credit Repair process was developed by experienced attorneys.

Speed. Documents are typically processed and sent out for investigation within 3-5 days.

Support. Award-winning customer service guarantees your satisfaction.